institutional kalman filter: dynamic true price estimation

Info

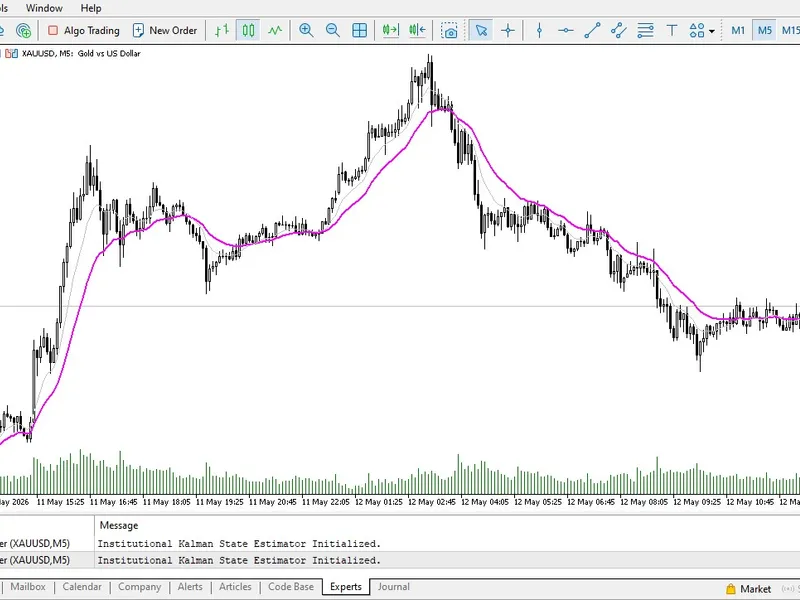

The institutional kalman filter: dynamic true price estimation is a Indicator for MetaTrader 5 that the flaw in static smoothingretail indicators, from moving averages to gaussian filters, rely on static lookback periods, treating each price tick as absolute. however, sudden liquidity sweeps by market makers distort these indicators, leading to false breakout signals that trap retail traders.

Usage

This tool is typically used for enhancing chart analysis and decision making.

Platform

This Indicator works exclusively on MetaTrader 5 (both build 600+ and newer versions).

Setup

Place the downloaded file in MQL5/Indicators folder via File ? Open Data Folder in MetaTrader 5.

How to Install and Use institutional kalman filter: dynamic true price estimation

1. Installation: Place your file in the MQL/Indicators folder via "Open Data Folder" and restart your terminal.

2. Loading: Find the indicator in the Navigator, drag it onto your chart, and configure the input parameters in the popup window.

3. Customization: Press Ctrl+I to open the indicator list, select your tool, and click "Properties" to change colors, levels, or visual styles.

4. Updating: Replace the old file in the Indicators folder with the new version and restart the platform to apply changes.

Frequently Asked Questions

Q: Why is my indicator not showing? A: Verify the file is in the MQL/Indicators folder, or try right-clicking the "Indicators" tree in the Navigator and clicking "Refresh."

Q: Do custom indicators slow down the platform? A: Too many complex indicators can impact performance; remove unused ones via the "Indicator List" (Ctrl+I).

Q: Can I use MT4 indicators on MT5? A: No, MQL4 and MQL5 are distinct languages; ensure the indicator is compiled specifically for your platform version.

What this tool does

the flaw in static smoothingretail indicators, from moving averages to gaussian filters, rely on static lookback periods, treating each price tick as absolute.

Typical Use Case

This Indicator excels in automated trading and technical analysis on MetaTrader 5.

Compatible Platform & Setup

This Indicator works on MetaTrader 5. Place the file in the MQL5/Indicators folder and restart the terminal.

Description & Settings

Related: Sniper Gold SMC Pro Plus: Institutional Smart Money Concepts Indicator for MT5 - another powerful indicator for MetaTrader 5 traders.

the flaw in static smoothingAlso recommended: institutional equilibrium matrix for mean-reverting assets - similar indicator with strong performance on MetaTrader 5.

retail indicators, from moving averages to gaussian filters, rely on static lookback periods, treating each price tick as absolute. however, sudden liquidity sweeps by market makers distort these indicators, leading to false breakout signals that trap retail traders.

the institutional edge: control theory

quantitative firms address this issue by employing the kalman filter, a mathematical algorithm used in aerospace engineering. this filter treats the price feed as a signal with 'measurement noise', aiming to extract the true market direction.

introducing the institutional kalman filter

this filter brings state-of-the-art estimation to mql5 terminals.

dynamic kalman gain

the filter calculates market uncertainty in real time. when volatility spikes, it adjusts its 'kalman gain', disregarding erratic price movements.

true price estimation

the algorithm separates the underlying trend (state) from high-frequency manipulation (noise), providing a smooth trajectory aligned with institutional intent.

zero static lag

as a recursive model, the kalman filter adapts tick-by-tick without arbitrary periods, based on defined process noise and measurement noise parameters.

implementation

deployment:

apply the indicator to lower timeframes (m1, m5, m15) to counter algorithmic liquidity sweeps and erratic spread changes.

noise filtering:

observe how the kalman line disregards manipulative price wicks, adhering to institutional order flow.

ea enhancement:

replace lagging moving averages with this dynamic estimator to prevent automated trades based on short-term market noise.

You may also like: institutional market reversal - the smart money concepts way - excellent alternative for indicator users on MetaTrader 5.

Source Code

#property copyright "robotfx"

#property link "https://robotfx.org"

#property version "1.00"

#property indicator_chart_window

#property indicator_buffers 1

#property indicator_plots 1

#property indicator_label1 "kalman true price"

#property indicator_type1 draw_line

#property indicator_color1 clrmagenta

#property indicator_style1 style_solid.......

⚠ Limitations & Risk Warning

- This tool is provided for educational and testing purposes only.

- Past performance does not guarantee future results.

- Trading involves substantial risk of loss. Use on a demo account first.

- Results may vary depending on market conditions, broker, and settings.

- We recommend thorough backtesting and forward testing before using with real funds.