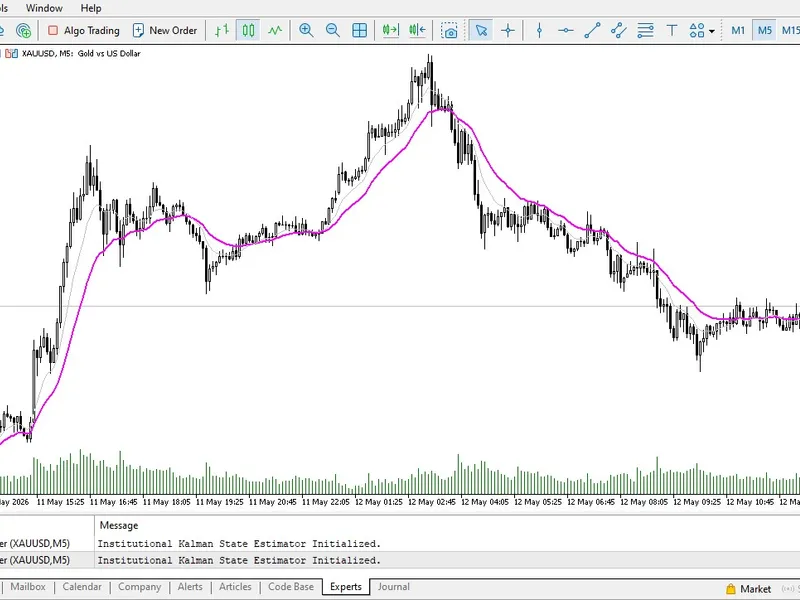

Institutional Kalman Filter (Dynamic True Price Estimator)

This is a powerful addition to your MetaTrader 5 toolkit designed to optimize market analysis and performance. This technical indicator acts as a specialized analysis tool designed to visualize market data. It helps traders identify emerging trends, momentum shifts, and key support or resistance levels by plotting statistical calculations directly onto price charts.

How to Setup and Use Institutional Kalman Filter (Dynamic True Price Estimator)

1. Installation: Place your file in the MQL/Indicators folder via "Open Data Folder" and restart your terminal.

2. Loading: Find the indicator in the Navigator, drag it onto your chart, and configure the input parameters in the popup window.

3. Customization: Press Ctrl+I to open the indicator list, select your tool, and click "Properties" to change colors, levels, or visual styles.

4. Updating: Replace the old file in the Indicators folder with the new version and restart the platform to apply changes.

Frequently Asked Questions

Q: Why is my indicator not showing? A: Verify the file is in the MQL/Indicators folder, or try right-clicking the "Indicators" tree in the Navigator and clicking "Refresh."

Q: Do custom indicators slow down the platform? A: Too many complex indicators can impact performance; remove unused ones via the "Indicator List" (Ctrl+I).

Q: Can I use MT4 indicators on MT5? A: No, MQL4 and MQL5 are distinct languages; ensure the indicator is compiled specifically for your platform version.

Description & Settings

The Flaw in Static Smoothing

Every traditional retail indicator—from Moving Averages to complex Gaussian filters—relies on a static lookback period. The fatal flaw here is that they treat every printed price tick as absolute truth. When institutional market makers engineer sudden liquidity sweeps (massive wicks), static indicators absorb this fake data, skewing their trajectory and triggering false breakout signals that trap retail capital.

The Institutional Edge: Control Theory

Proprietary quantitative firms treat the broker's price feed as a signal corrupted by "Measurement Noise." To extract the actual market direction, they utilize the

Kalman Filter

—the exact recursive mathematical algorithm used in aerospace engineering for missile guidance and orbital navigation.

The

Institutional Kalman Filter

brings continuous state estimation to your MQL5 terminal.

Core Quantitative Architecture

Dynamic Kalman Gain:

Instead of averaging past prices, the engine calculates the real-time uncertainty of the market. If volatility suddenly spikes erratically, the algorithm instantly lowers its "Kalman Gain," mathematically ignoring the fake price wicks.

True Price Estimation:

It seamlessly separates the true underlying trend (State) from high-frequency manipulation (Noise), plotting a flawlessly smooth trajectory that tracks institutional intent.

Zero Static Lag:

Because the Kalman Filter is a recursive predictive model, it requires no arbitrary "Period" inputs. It adapts tick-by-tick based on mathematically defined Process Noise and Measurement Noise parameters.

Execution Protocol

Deploy the Engine:

Attach the indicator to lower timeframes (M1, M5, M15) where algorithmic liquidity sweeps and erratic spread widenings are most frequent.

Filter the Noise:

Observe how the Kalman line completely ignores sudden manipulative price wicks, staying absolutely faithful to the core institutional order flow.

Upgrade your EA:

Replace your lagging moving averages with this dynamic state estimator to ensure your automated systems never execute a trade based on fake, short-term market noise.