Institutional GA R C H(1,1) Volatility Forecaster

This professional-grade solution for MetaTrader 5 helps traders achieve greater efficiency in their daily workflow. This technical indicator acts as a specialized analysis tool designed to visualize market data. It helps traders identify emerging trends, momentum shifts, and key support or resistance levels by plotting statistical calculations directly onto price charts.

How to Setup and Use Institutional GA R C H(1,1) Volatility Forecaster

1. Installation: Place your file in the MQL/Indicators folder via "Open Data Folder" and restart your terminal.

2. Loading: Find the indicator in the Navigator, drag it onto your chart, and configure the input parameters in the popup window.

3. Customization: Press Ctrl+I to open the indicator list, select your tool, and click "Properties" to change colors, levels, or visual styles.

4. Updating: Replace the old file in the Indicators folder with the new version and restart the platform to apply changes.

Frequently Asked Questions

Q: Why is my indicator not showing? A: Verify the file is in the MQL/Indicators folder, or try right-clicking the "Indicators" tree in the Navigator and clicking "Refresh."

Q: Do custom indicators slow down the platform? A: Too many complex indicators can impact performance; remove unused ones via the "Indicator List" (Ctrl+I).

Q: Can I use MT4 indicators on MT5? A: No, MQL4 and MQL5 are distinct languages; ensure the indicator is compiled specifically for your platform version.

Description & Settings

The Mathematical Flaw in Retail Volatility (ATR)

Retail algorithms universally rely on the Average True Range (ATR) to calculate stop-losses and position sizing. This is a fatal structural flaw. The ATR is purely backward-looking—it merely averages past price movements. When macroeconomic shocks occur, the ATR lags significantly, leaving your capital exposed during the exact moments when dynamic protection is needed the most.

The Institutional Standard: GARCH(1,1) Model

To survive dynamic market regimes, top-tier quantitative hedge funds and options pricing desks do not look at past averages. They forecast future variance using

Generalized Autoregressive Conditional Heteroskedasticity (GARCH)

.

The

Institutional GARCH(1,1) Forecaster

brings this Nobel-prize-winning econometric mathematics directly to your MQL5 terminal.

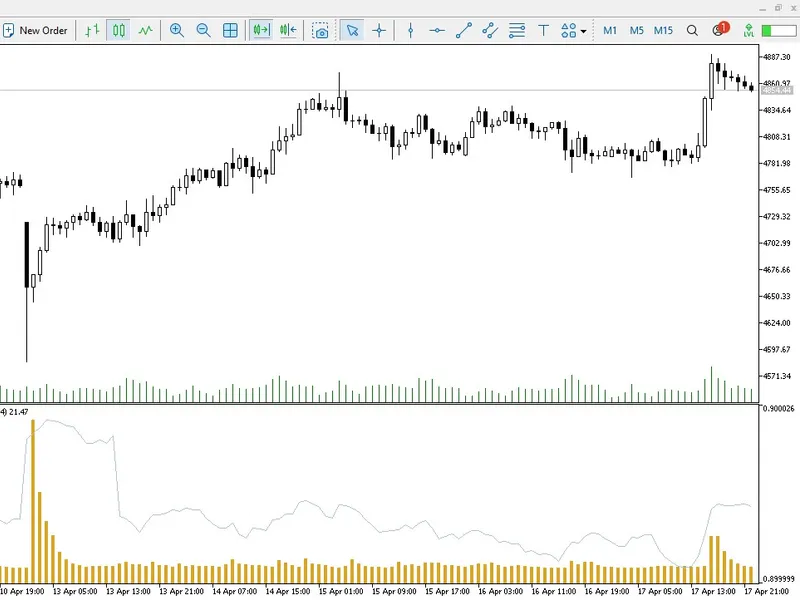

Core Quantitative Architecture

Predictive Variance:

Instead of averaging past ranges, the algorithm calculates logarithmic return shocks (Alpha) and historical volatility persistence (Beta) to forecast the exact mathematical probability of variance for the next execution candle.

Non-Lagging Risk Assessment:

Instantly detects volatility clustering (the tendency for large moves to be followed by large moves), allowing your Expert Advisor to preemptively widen trailing stops before the ATR even begins to react.

Institutional Default Weights:

Pre-configured with standard Wall Street econometric parameters ($\alpha = 0.09$, $\beta = 0.90$) to model typical financial asset decay, with full inputs exposed for advanced parameter optimization.

Zero External Dependencies:

Calculates complex logarithmic arrays natively in C++, bypassing the need for sluggish external Python integrations.

How to Implement in Algo-Trading

Drop the ATR:

Stop using static period averages for your dynamic stop-losses.

Forecast the Shock:

Monitor the GARCH histogram. A sudden spike indicates a high-probability volatility shock is mathematically imminent.

Protect Capital:

Use this indicator's buffer to dynamically shrink your lot sizing (VAPS) or widen your stop-loss milliseconds before a major liquidity injection sweeps the retail order book.